Why Credit Cards??

Credit Card is one of the most popular financial product across the world and is witnessing a huge growth rate. Few of the reasons for this are:

- Access to Credit & opportunity to upgrade your purchase

- Ease of usage & protection against robbery, theft

- Additional incentives for usage of cards like Rewards, Cashback etc

- International acceptance

Why Islamic Banking??

Islamic Banking helps take care of one of the most important financial requirement of Muslim world: To avoid Riba & Haram products. There are many other advantages too.

- Avoidance of Riba (Riba; Interest is Haram for Muslims)

- Avoidance of Haram product: There are many products & purchases which have been earmarked as Haram or banned.

- Help avoid undue exposure to debt & debt traps

- Helps with ethical banking for all

Enters the Islamic Credit Card:

Islamic Credit Card follows the guidelines of Islamic scholars and help provide a financial solution which brings the best of both the world. The concept of Islamic Credit Card is cool even for the non-Mulsim world. In fact, this can become the bridge long due between the conventional retail banking & Islamic banking for people of all faiths.

Major perceived advantages of Islamic Credit Card:

- Ethical banking solution to larger community

- Avoidance of risky & illegal purchases like Gambling etc.

- As Gharara is banned, so better access to credit without the fear of compounding interest

- Nil to lower cost of fund compared to traditional Cards

So what is the current status & challenge??

Islamic credit card is one of the most controversial product currently in the Islamic fintech market. While Credit card as a product has become a necessity across the world, a lack of clarity and acceptance of a credit card product under Shariah compliance board act a major impediment for retail popularization of Islamic banking system.

First Islamic credit card was launched in Malaysia in 2002 under the Bay’ al’ Inah model wherein the customer buys a commodity from bank with a deferred payment and sells it back to same bank as cash. The Customer now uses the cash for purchases. This model has been rejected by most of the academia as being a gimmick for riba avoidance. This model is still being followed in SE Asia with many banks offering Credit Cards under this model.

The Gulf countries decided to give a pass to Bay al’-Inah and instead focused on Tawarruq which is similar to the previous model but herein the customer buys a commodity from bank at a cost+ model with deferred payment and then sell it to a third party at immediate cash price. A Wadiah account is created by the bank as a guarantor wherein the customer deposit this money or the third party deposit on behalf of customer. While the bank manages the facility, the customer can use the Card with the limit upto the deposited amount.

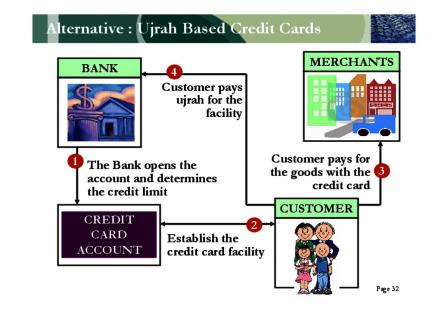

HSBC has tried with the Transaction fixed fee based card (Ujrah) wherein they are charging the customers for various services availed and no interest was charged from the customer. They are also charging the seller for the services.

The Road Ahead:

The Islamic credit cards have been a major driver in Malaysia, Indonasia, UAE & major gulf countries. We have seen an interest from Pakistan, Bangladesh, UK & other countries. We are also seeing innovations like Takaful Credit card with integrated insurance and cards for extra credit during emergencies. There have been consumer studies revealing that while the acceptance of a Islamic credit card is higher for Muslim population, the differentiator is the level of advertisement and brand outreach.

There are two ways to grow from here:

Inorganic growth through Fintech disruptions: New Islamic fintech launch unique and attractive product bringing in huge disruption in the market and grabbing a larger market share

Organic growth through conventional banks creating newer products in Islamic credit cards pushed with promotions to bring in unbanked or underbanked customers. (A recent study shows a low level of card penetration in most of the Muslim countries; Around 10-15% of these people had avoided credit card due to Islamic philosophy).