A 2 Billion Unbanked population opportunity worth $10 Trillion+

World over, there are more than 2 Billion unbanked people without proper access to financial products & solution. This is one of the major impediments in poverty reduction and social-economic balance in the society. Out of these, close to 800 millions are Muslim population who are largely unbanked across the world. The condition is much worse for woman.

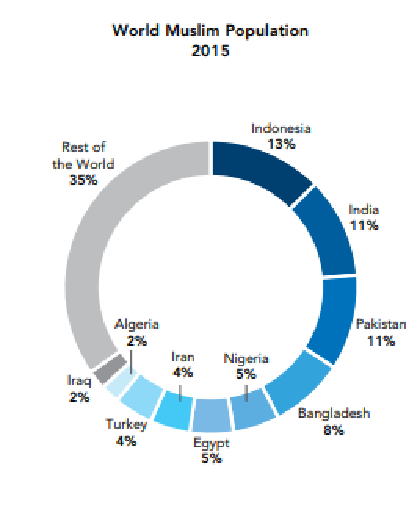

Muslims population has larger footprints in Asia with top 3 countries: Indonasia, India & Pakistan, accounting for 1/3rd of the total population. One of the major reason for voluntary absenteeism from banking is lack of Sharia compliant products in these markets. Close to 100M people have stated that lack of Islamic financial product reach as the reason for being ubanked. With a young and tech savvy population, Islamic Fintech can usher in an era of revolution for the segment.

Islamic fintech is expected to play the key role of bridging the gap between the large banking groups with limited maneuverability for differential financial systems and the unbanked / underbanked customers.

Islamic Banking & Finance system: How is it different??

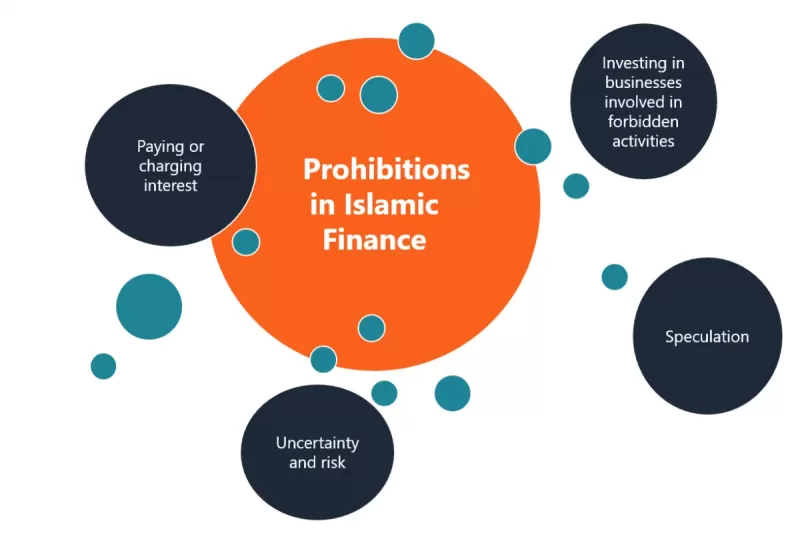

Islamic Banking is based on the philosophy of Shariah which provides specific guidelines for transactions with the purpose of creating socio-economic equality, prohibiting gambling, and interests among others.

Key Principles of Islamic Banking:

- Riba (Interest/Usuary): Riba is strictly prohibited in Islam. As Islam consider this as exploitive practice

- Haram (Prohibited): Investment / Finance in activities considered haram are strictly prohibited

- Maisir (Speculation): Speculations & gambling is strictly prohibited in Sharia.

- Gharar (Uncertainty / risk): Participation in activities with excessive uncertainty & risk is strictly prohibited. This effectively rules out Futures, derivatives etc.

- Material finality of transaction: Each transaction should have a real underlying economic transaction

- Profit / Loss sharing: All transactions should be equal in risk sharing and profit/loss the both buyer & seller.

“The Qur’an prohibits riba, which literally means “increase”. Technically riba is the increase when liquid or fungible assets (cash, debt, grains, etc.) are exchanged other than at par value.” -wikipedia

Understanding the difference between Conventional & Islamic Banking

Products & Services in Islamic Finance

Profit & Loss sharing

- MUDARABAH

- MUSHARAKAH

- MUSHARAKA AL-MUTANAQISA

Asset Based Contract

- MURABAHAH

- BAI’ MUAJJAL

- BAI’ AL INAH

- MUSAWAMAH

- ISTISNA & BAI SALAM

- IJARAH

- TAWARRUQ

For more details on these products, please refer here.

Modes Bases on Contract Safety & Security

- HAWALA

- KAFALA

- RAHN

- WAKALAH

- WADIAH & AMANAH

- QARD

Non-Banking Products

- SUKUK

- TAKAFUL

- ISLAMIC CREDIT CARD

- ISLAMIC FUND

- ISLAMIC DERIVATIVES

- SWAPS

- MICROFINANCE

How Fintech helps with Islamic Banking

Fintech implementation in IB: Blockchain for sukuk

“To address high costs and a lack of transparency within the sukuk market, blockchain could literally be the missing link” – Mr Damak, S&P Global Ratings.

He expects blockchain technologies will open the market to smaller companies by cutting the cost of issuing a sukuk. In 2019 an Indonesian microfinance institution, BMT Bina Ummah, used a platform created by startup company Blossom Finance to raise US$50,000 in what it claimed to be the first blockchain sukuk

Wahed Investments: World’s first Shariah compliant ROBO-Advisory firm based in US. Reached out to the underbanked Muslim population in US: “Wahed Invest seeks to make Shariah-compliant investing more efficient, charging lower fees than existing Islamic Finance investment managers, and more accessible, planning to make the platform available to Muslims globally, with low minimum investment amounts requirements” – Case Study, GIFR

Let’s understand the Islamic Fintech Landscape

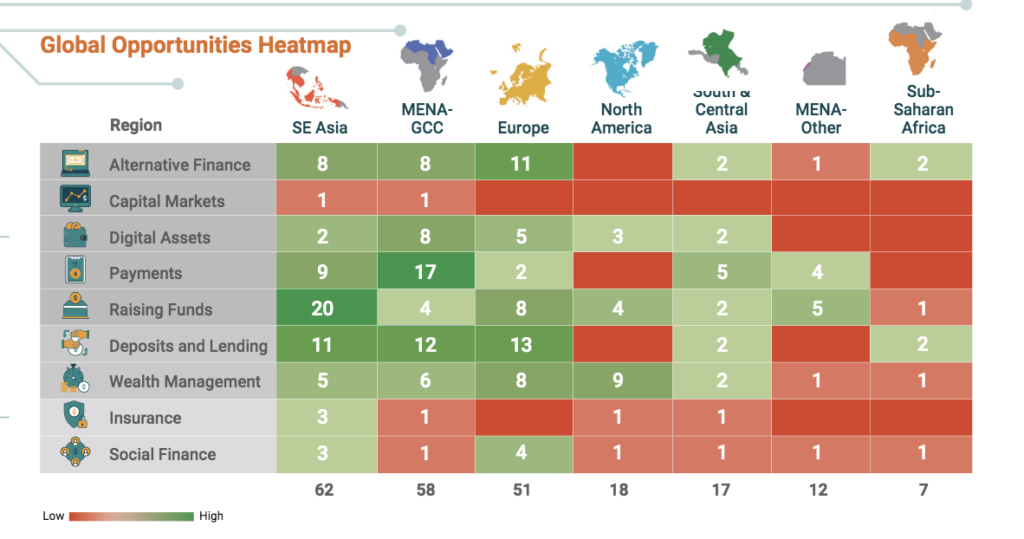

Islamic fintech market are predominantly existing in Asia with major contribution coming from OIC nations. Within this group, Saudi Arabia continues to dominate with close to 40% contribution, followed by Iran, UAE, Malaysia & Indonasia. There is a huge opportunity lying in Indonasia with its vast devoted Muslim population which is largely unbanked/ underbanked. Within the OIC, certain Central Asian countries like have started showing great traction for Islamic Fintech.

“Islamic fintech has become the fastest growing segment of financial technology among the Organization of Islamic Cooperation (OIC) countries. It is estimated that Islamic fintech in OIC countries accounted for $49 billion in transaction volumes in 2020” – GIF 2021 report.

Islamic Banking in India: An untapped opportunity: While much of the focus is there on MEASA & other OIC partners, India is one market with close to 11% of the world Muslim population which is completely untapped. As per the India’s central Bank RBI, Islamic banking is currently not pursued as medium in India. There is a clear requirement for easy access to finance for the poor and Islamic banking with Zakat & profit sharing rules can be a big boon here even to non-Muslims. World over, a large chunk of Islamic banking users are non-Muslim and as such the implementation of this will bring in an alternative medium for people. The added advantage is that many direct investors from GCC countries are looking at Shariah compliant finances to put in direct FDI and this is generally routed via third country in absence of a defined Islamic Banking system. With regular banks, it will be difficult to adjust to the rules and Fintech can leverage these to become global player in this segment.

Future of Islamic Fintech & The Covid Impact

Like it’s big brother, Islamic fintech market has also seen a sea change in 2020, mainly due to Covid led lockdowns and an urgent need for digital financial solutions. This has led to an spurt in investment in the sector by new as well as established banks and as per estimate it is expected to grow at 21% CAGR till 2025. The period also saw a major dip in investments as well as consolidations among big banks in this sector. One of the major M&A deal was Dubai Islamic Bank buying out Noor bank to create the world’s largest Islamic lender with $75B under assets.

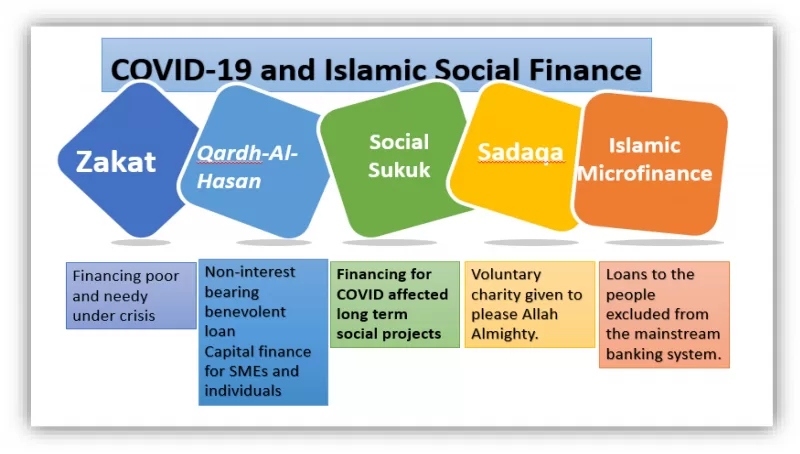

Covid-19 also led to an increase in Islamic social finance with multiple new products to take care of needy & poor.

Islamic Fintech market is poised for a huge growth and Banks & financial majors should ignore it at their own expense. In Non-OIC markets like Africa, Central Asia, Europe, US & East Asia, Shariah compliant products are gaining interest. With close of 3B population expectation for Muslim community by 2025, this represents a good 70% jump from 2015.

Islamic Banking can also be the tool in poor economies to give access to underbanked with support from rich thanks to the Islamic social finance support system.

Note: All images belongs their respective copywrite owners and any miss in crediting is purely by chance.