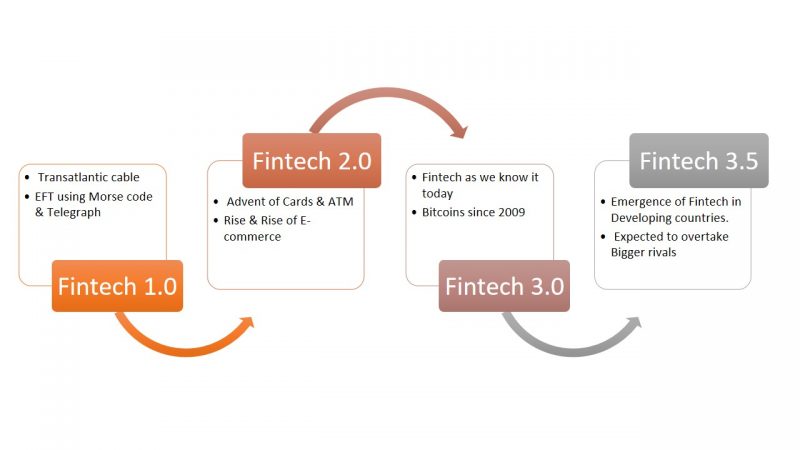

FINTECH 1.0 (1866-1967)

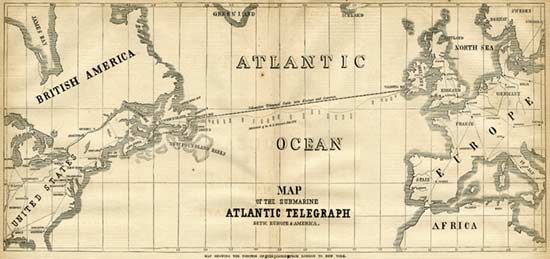

Fintech history dates back to the 19th century and even before that. In 1860, a device called PENTELEGRAPH was developed to verify signatures by banks. Historians accept 1866 as the first valid fintech footprints. This was the year the transatlantic cables were setup leading to an era of creating network infrastructure & linkages around the world. Setting up of Electronic fund transfer through Telegraph & Morse code in 1918 by Fedwire led to first baby step in digitalization of money. The two WW also saw a new set of coders & codebreakers mainly for the military purposes (though this set up the idea of coding & future digital development). The publication of book “The Economic consequences of Peace” in 1919 is treated as the first thought on the fintech driven future.

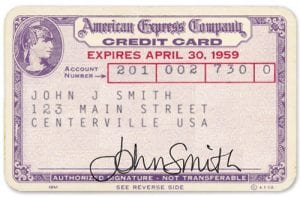

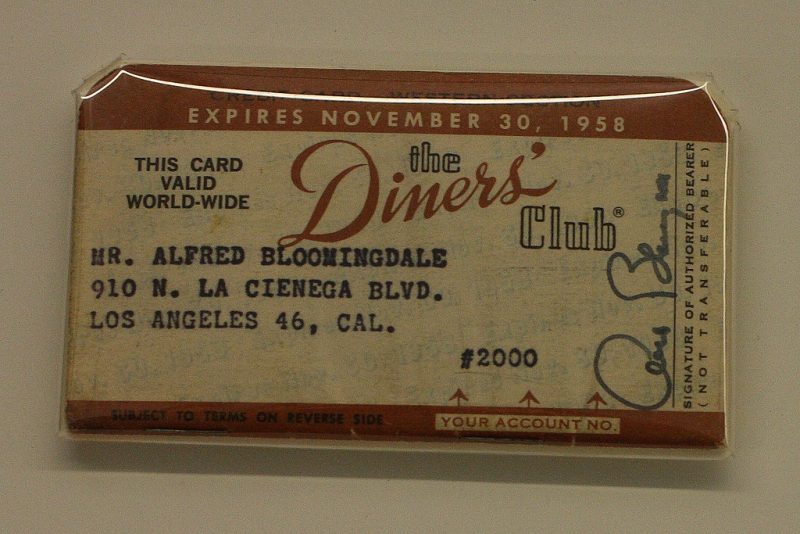

Generally, Fintech historians miss one important and life altering event of Fintech 1.0 and that is Diner’s Card in 1950. This was first honest effort to make your payments cashless and while the beginning was humble and limited to restaurants payments, it paved the way for future to develop. This was followed by introduction of Credit Card by Amex in 1958. With introduction of Screen based stock data by Quotron in 1960, the Financial market took the huge stride, one major successful implementation of early fintech ideas.

FINTECH 2.0

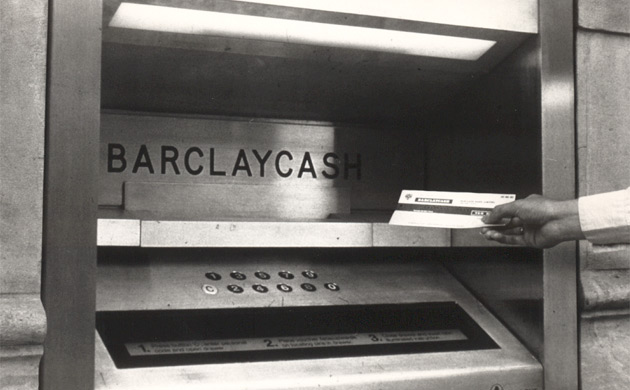

Fintech 2.0 is considered to begin with the introduction of ATM machine by Barclay’s in 1967. Just the year before in 1966, Telex had replaced Telegraph for transferring information across the world; thus heralding an era of connected financial transactions & communication.

The major fintech growth came in 1971 with setup of NASDAQ as the first Electronic stock market. It changed the way bidding is done and modernized the IPO process significantly. This is considered as one of the most important Fintech development of all times. This was followed by introduction of SWIFT in 1973, another revolutionary service standard. The 80’s saw the development of electronic trades and online banking systems. Tradeplus (E-trade) introduced the E-trade for the first time in 1982 for it’s customers. This was followed by NBS /WF offering online banking to their customers by 1983/1985. Today, we can’t imagine a world without these two technology services in our life. 1983 was the year, when Mobile phones were launched for the first time too. The development of complex computing systems helped in launching of newer and more dynamic processes & products. One major breakthrough was the evolution of E-commerce during the mid 90’s which made the reliance of digital finance much more significant. 1998 saw the launch of PAYPAL, the pioneer of cashless payments in years to come.

The Y2K bubble burst and subsequent years saw a rapid development of technology in financial sectors, mainly being deployed by the traditional banks as a support function to their primary channels. The 2008 financial crisis led the fundamental change in the outlook towards the Fintech sector and the need of innovation led to the real boom that unveiled in the coming years.

FINTECH 3.0

The 2008 crisis led to the following requirements

- Post crisis reforms required stricter regulatory compulsions for traditional banks and it opened up a new market for smaller players. This was further helped by mistrust of public in large financial institutions

- Overall focus of the industry was on cutting down operational cost using technology

- Advent of new technologies like P2P, Wallets, Bitcoins led to ease of use for the general consumer

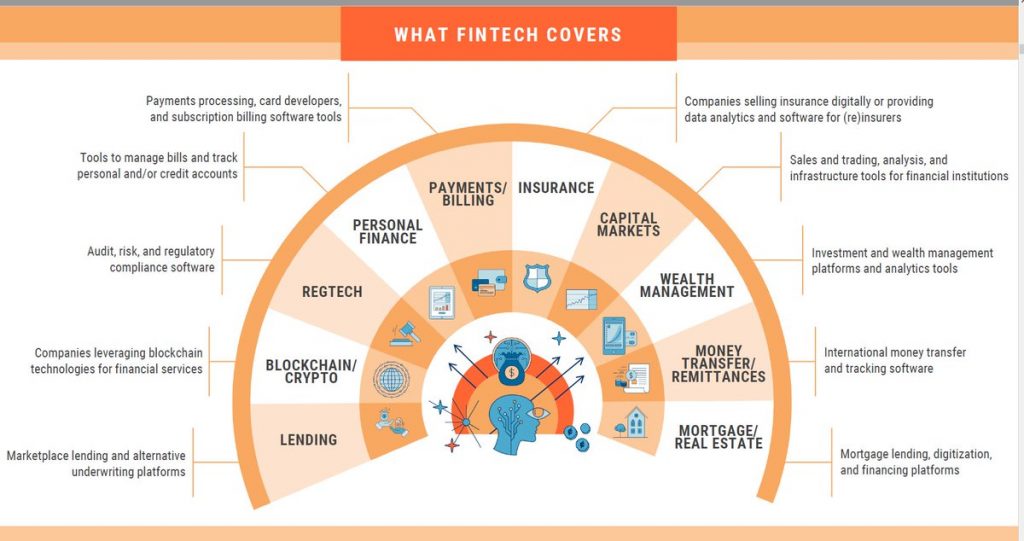

These requirements and developments led to a new era of Financial services and to FINTECH as we know it today. Two major events were development of Bitcoin in 2009 as the first cryptocurrency and P2P payment systems in 2011. The western world has been churning new developments and hundreds of new unicorns since then. BaaS, RegTech, Digital Lending, InsurTech, Wallets and many more segments are seeing growth and innovations on a daily basis.

FINTECH 3.5

The year 2014 onwards saw a non linear rise of two most populous countries in Fintech; namely China & India. Devoid of large chains of complex physical banking infrastructures, these two countries saw a very fast paced growth in the Fintech sector. This along with Fintech developments in Africa is considered as the growth engine for 2014-2018. This is led by SaaS developments like Financial software by Indian IT companies, m-Pesa in Africa, Payment banks in India, Alipay in China to name a few.

Please find below a snapshot for Fintech Evolution