According to Statista & UN, 26% of the world population is below the age of 15 years (roughly 2 billion people worldwide), and 16% is between 16-24 years!!!

Youths & kids are one segment which has never got any serious attention from traditional Banks and other old school financial services companies. According to a recent UN study, youths are 44% less likely to have access to financial products.

But why so?

- Regulatory requirements: Countries have different age criterion for access to formal banking process. Most countries don’t allow access to formal banking before 18-21 years.

- Lack of financial maturity: This segment is traditionally considered to have low maturity for financial freedom and can lead to debt trap.

- Lower financial power: Youth and kids below the age of 24 won’t have high income source as they are either dependent on parental income or have just started earning.

- Limited access & parental guidance: In most geographies, youths’ financial decisions are still governed by parental guidance and they have limited opportunity to spend independently

- Accusation threat of profiteering for Financial companies: The companies are at higher risk of being accused of making undue profits from under educated and gullible kids & youth

These factors make the youth and kids financial market slightly unattractive for the traditional market players and can be gauged from the fact that only 46% of the youth have formal access to financial services against 66% of adults as per another UN study. They may be missing the bus and of course, the opportunity of access to 3+ billion potential customer base.

There are many positives of this market for Banks & other financial players:

- Access to newer untapped market

- Potential to grow the volumes multifold with age and increase in income

- As youths are more open to experiment, opportunity to offer diverse product innovations

- Lower cost of customer acquisition and increased customer loyalty

- Opportunity for cross-sell and higher profitability

Youth financial products should have additional adjustments (source: (PDF) BANK PRODUCTS AND SERVICES FOR CHILDREN, YOUTHS AND YOUNG ADULTS: FEATURES, MODELS, CUSTOMIZATION (researchgate.net))

- Keep financial, social and cyber security of young people, and be adjusted to the level of knowledge and the ability of young people to understand the principles of their functioning,

- Be free of charge or generate low costs not affecting the safety of young people,

- Be adjusted to the age of young people, meaning they “grow” together with them,

- Be available independently on the economic situation of young person,

- Bring value added (increase knowledge, financial, internet and life skills)

- Not require to bind the client with the bank to use in the future other and more advanced products and services,

- Give a sense of stability and security to young people,

- Provide constant access to savings anytime and anywhere,

- Are offered through communication channels preferred by young people,

- Allow to use helpdesk or helpline in a form suitable for young people (chat, video call).

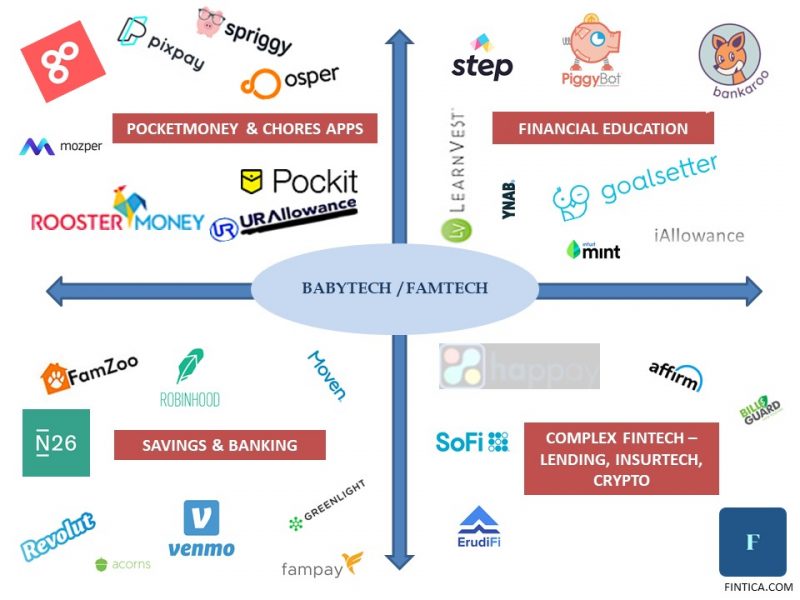

Youths & kids market can be divided into what is commonly termed as Gen Y (1990-2000, Age 20+), Gen Z (2001-2010; Age10+), Gen Alpha (2011+; <10 years). The requirements & usage for each group is very different from one another and we have following product types being offered currently by traditional and new players

- Pocket money tools for managing finance

- A subcategory is getting paid for doing small chores

- Saving tools for small savings

- Financial education tools

- Access to complex financial tools & products like lending, trading

Let’s see the generation wise expectation of financial understanding:

| GEN/ Expectation | What is expected | Usages | Importance | Financial options |

| Gen Alpha | Understand the importance of finance & money | Intial saving habits & pricing understanding | Importance of saving & impact of careless spends | Money Saving and basic financial educational tools. First level access to financial products |

| Gen Z | Basic usages of financial tools and learning of products | Budget planning. Expense planning. Basic wallet expenses. School expenses | First hand access to world of financial product and initiation of steps towards financial freedom | Basic pocket money tools, Savings, basic payments & complex financial educational tools |

| Gen Y | Usage of Mobile & internet to access medium to complex financial products | Extensive usage of financial products for daily consumption | Full access to full spectrum of financial product and stepping into the world of financial freedom | Access to Savings, lending apps, Wallet, BNPL, Online payments, Insurance |

The advantage with Gen Z & Gen Alpha over previous generations are them being extra tech savvy and financially sound for their age (Partly due to the Financial crisis of 2008-10). This coupled with awesome access to internet and mobile makes them a great target for the new generation companies.

Enter the Fintech companies with focus on tech and innovations. With limited to no baggage of policy hurdles, conducive environmental factors, and access to more youths thanks to increased mobile & internet penetration; they have changed the way, youth & kids perceive finance. There are many innovative and challenger products across categories that have flooded the markets thanks to fintech revolution.

- Revolut: Revolut Junior is changing the rule of the game with Teens as target audience (Age 7+). Currently, it is being run with parental guidance but the financial freedom is going to be soon in the hand of the spenders.

- Acorns: Acorns is a great saving tool for youth wherein it invest the rounded off money for each purchase basis your profiling.

- Famzoo: Famzoo provided prepaid card and financial education for kids and teens.

- Gohenry: Gohenry offer subscription based Pocket money apps which are very popular among wealthy teens & youths

- Osper: Similar to Gohenry, Osper also offers pocket money app at a fixed monthly rental aimed at upper middle class youth

- Spriggy: Spriggy is a very popular pocket money and financial education app for youth and parents

- Rooster Money: Roostermoney is a free kid’s allowance and chores app. It let’s kids earn money against small chores asssigned to them by parents

- Fampay: Fampay is India’s first card aimed for youth. Considering the large base, this might become a huge challenger fintech

- Pixpay: Pixpay is a great french startup for teens (10+) for managing and spending their pocket money. It lets parents replace a pixpay debit card for cash.

- Affirm: Affirm is a great enabler for youth with its BNPL at retail POS with instant approval

- N26: N26 was the early innovators with their app “Papaya”. They are still youth friends and very popular in Germany and Europe.

- Robinhood: Robinhood is a great platform for young brains to try their hands in trading and has a strong base among young adults.

- Learnvest: While closed down now, it was a great initiative for providing financial education for youth and kids

- Pockit: Pockit is an English prepaid accounts mobile first app meant for the unbanked and youth customers

- URAllowance: URAllowance is a great double sided digital currency platform powered by URA token with one side as kids and other as parents.

- Moven: Moven is a great tool for youth to understand their spending patterns. It is a real-time mobile money app and is hugely popular among youth

- Venmo: With Paypal as owners and great interoperability & connectivity to multiple bank and card accounts, Venmo is gaining traction among youths at a much faster pace.

- Happay: Happay is a great expense management solutions for helping the youth and enterprise

- SoFi: Sofi targets graduate students with student loans, mortgages and credits.

- BillGuard: BillGuard is a great tool to ensure security for your payments

- Greenlight: One of few Unicorns focusing on kids spending habits using smart debit card. Valued at 1.2B$

- Mozper: Mexican startup of digital pocket money app for children

- Step: A teen mobile banking app with focus on financial education (Age:13-18)

- BusyKid: A new app for Financial education and managing daily chores system for kids

- ERNIT: A mobile app program that provide a digital piggy bank for kids

- EarlyBird: A fintech gifting platform for parents and kids

- Pennybox: An Australian fintech platform for financial education for kids

- Goalsetter: An education first banking app for young children

- Erudifi: Fintech firm offering collateral-less student loans

- Junio: India’s one of the first Fintech pocket money app for the kids

There has been great interest in the Babytech & Famtech sector currently with more than $350M raised in 2020 alone and $600M overall in 100+ deals. The sector becomes huge if you add in the retail tech specialized for kids. Current market size for the sector is expected to be way beyond $50B worldwide.

The Famtech & Babytech market is shaping up and while the failure rates might be high initially, this is one sector which is going to mint unicorns like no other.

~ Fintica